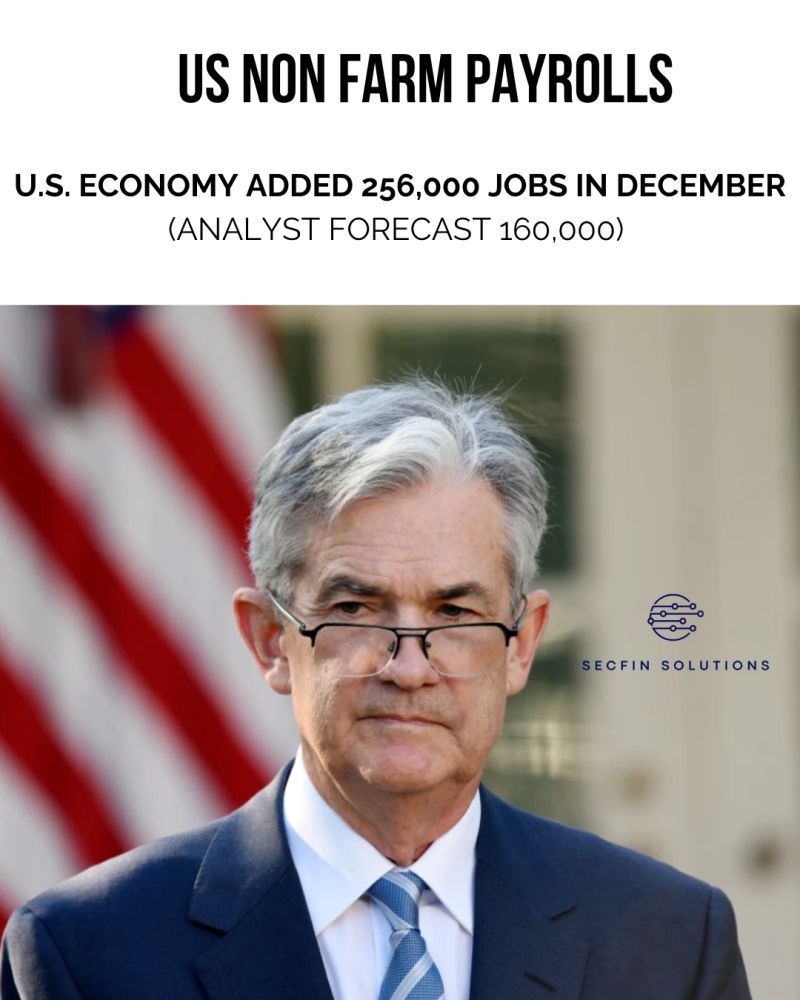

Yesterday’s U.S. Non-Farm Payrolls report delivered another upside surprise, showcasing the extraordinary resilience of the American labour market. Despite tightening financial conditions and the cumulative effects of higher interest rates, hiring remains robust, and wage growth is steady. Once again, the U.S. economy is challenging expectations of a softening growth trajectory.

For central bankers, this is a conundrum. The Federal Reserve Board has been clear that its priority is taming inflation, but with the labour market so strong, the risk of a second wave of price pressures looms large. While markets may be pricing in a “pause and hold” narrative, yesterday’s data suggests the Fed may need to keep the door open to further tightening.

The implications for global markets cannot be ignored. Treasury yields have already reacted, but the message from this report is clear: higher for longer is not just a theory, it’s becoming reality. The repricing of risk assets and fixed income markets could still have a long way to go, and any expectation of a pivot to rate cuts feels increasingly premature.

For the UK, the challenges are just as significant. Inflation, particularly in services, remains stubbornly high, and economic growth is fragile. The Bank of England must now contend with external pressures from a strong U.S. economy, a potential re-acceleration of global inflation, and rising Treasury yields, which will inevitably spill over into gilt markets.

I believe we are far from the peak in yields, particularly in the long end of the curve. Even at current levels, I would be outright short 10- and 30-year gilts. The risk/reward of expecting a rally in UK fixed income seems increasingly skewed, and we may still see significant repricing as global realities set in.

Meanwhile, Rt Hon Rachel Reeves is in China this weekend, navigating complex discussions about trade, investment, and the UK’s role in a rapidly shifting global economy. As Chancellor, she faces a daunting balancing act: how to support domestic growth while responding to external challenges like these and ensuring long-term fiscal stability. It’s a weekend of tough thinking for policymakers, to say the least.

The bigger question for markets is whether we’ve underestimated the staying power of high rates. Yesterday’s data points to an economy more resilient than expected, a labour market that refuses to slow, and a yield curve that likely hasn’t reached its peak.

What are your thoughts on yesterday’s employment report and the global implications? Are we prepared for what could be a prolonged period of higher yields? Let’s discuss.

SecFin Solutions

Want to be notified about all my posts? Ring my bell 🔔

SecFin Solutions Education and Consulting Services

https://lnkd.in/dfQyAQpZ